Disclaimer: The information provided in this article is for educational and informational purposes only. It should not be considered financial, investment, or legal advice. Readers are encouraged to consult with qualified professionals before making financial decisions.

That’s the foundation of financial awareness, and yet it is often overlooked inside families. We speak about grades, health, and careers, but do we truly talk about budgeting, saving, or debt? A surprising number of households never do. According to a FINRA survey, only about 37% of U.S. adults could correctly answer at least four out of five financial literacy questions. That statistic highlights a gap. A gap that you, as a family member, can begin to help close.

Conversations drive change. The first step is not teaching formulas or handing over spreadsheets. It’s about making money talk as natural as discussing dinner plans. Why? Because silence creates myths, and myths fuel mistakes. Families who avoid the topic often see members fall into credit traps, live paycheck to paycheck, or lack confidence to make everyday financial choices. A deliberate shift—asking open-ended questions, sharing stories, admitting past mistakes—turns financial literacy into a family norm.

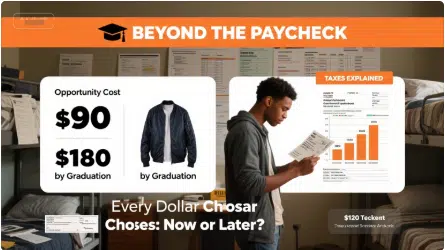

Meet Emily, a 16-year-old high school student. Her parents noticed she kept asking for money to buy sneakers, coffee drinks, and phone accessories. Instead of lecturing, her mother gave her a prepaid debit card with a fixed monthly allowance. The rule was simple: once the money was gone, it was gone.At first, Emily overspent in the first week. She was frustrated. But the next month, she began tracking purchases using a free budgeting app. By the third month, she proudly told her parents she had $20 left over. What changed? A controlled environment, small failures, and quick feedback.Parents sometimes fear giving teens financial responsibility. Isn’t it risky? What if they waste it? In truth, small mistakes with $50 are far safer than large mistakes with $5,000 in adulthood. The earlier the exposure, the greater the long-term confidence. Family-friendly tools and apps now make this process easier by combining allowance management, goal setting, and spending insights in one place.

Numbers need transparency. Families often hide bills, salaries, or mortgage details. The intention may be noble—protection from stress—but the outcome is ignorance. When adult children suddenly need to manage rent, loans, or insurance, they are shocked. By sharing, parents model responsibility and realism. For example, showing the monthly electricity bill helps younger members understand why “turning off the lights” is not nagging but saving.Transparency also works across generations. Imagine a grandfather explaining how he handled his pension, or an aunt showing how she refinanced her mortgage. Such stories turn abstract terms like “compound interest” into relatable lessons. Knowledge passed down becomes wealth preserved.

Consider Daniel and Sofia, both in their late twenties. They enjoyed dining out, traveling on credit, and shopping impulsively. Within three years of marriage, they had $18,000 in credit card debt.When Sofia’s older brother saw the stress mounting, he didn’t criticize. Instead, he invited them to a “family finance night.” They ate pizza, opened laptops, and reviewed their monthly expenses line by line. The biggest surprise? Nearly $600 each month went to delivery apps and coffee shops.The solution wasn’t deprivation—it was redirection. Together, they agreed to cook at home three nights per week, switch to cash envelopes for discretionary spending, and set up automatic debt payments. Within 18 months, their debt shrank to less than $3,000. Today, they still host “budget dinners” every quarter, inviting relatives and friends to join. What began as a gentle intervention turned into a sustainable habit.

Books, websites, and podcasts can add authority when family advice feels too personal. Sometimes, relatives resist hearing from each other. But when a reputable source echoes the same principles, the message sticks. For example, pointing a sibling toward free educational platforms like Investopedia’s Budgeting Basics or articles from trusted financial magazines can provide neutrality and professionalism.

Podcasts and online talks that share real-world financial struggles and solutions remind listeners that they are not alone—and that positive change is possible. With regular exposure, family members internalize the idea that resilience is built step by step.

Wealth involves mindset. Too often, families equate money with secrecy, shame, or power. But reframing it as a tool for freedom creates healthier dynamics. Ask yourself: do my children know the difference between assets and liabilities? Do my siblings understand why life insurance matters? When the mindset changes from “money is stressful” to “money is empowering,” family culture shifts.Even small rituals—like celebrating when someone reaches a savings goal, or discussing financial news over Sunday dinner—can normalize the subject. In fact, many households conduct annual “financial retreats,” where members review budgets, charitable giving, and investment performance. This is not arrogance—it is preparation.

Now, consider Marcus and Elaine, retired teachers in their late sixties. Their adult children assumed they had “enough” because they owned a house and had pensions. But when medical bills increased, Marcus and Elaine admitted their savings were thinner than expected.Instead of hiding, they called a family meeting. Together, they reviewed healthcare options, long-term insurance policies, and estate planning documents. At first, their children were uncomfortable. Talking about wills and inheritance felt grim. Yet by the end, they all felt relief.The parents gained support in navigating Medicare. The children learned how trusts work. More importantly, the family avoided potential conflicts. This case underscores the value of intergenerational honesty. Discussing money at later stages of life ensures smoother transitions and better preparation.

Consistency builds resilience. One-time lectures rarely work; ongoing habits do. Encourage family members to:

- Track spending weekly.

- Set up automatic savings transfers.

- Share goals openly (e.g., “I want to buy a house in five years”).

- Celebrate small wins.

These rituals reinforce discipline. Over time, the once-taboo subject of money becomes second nature, just like brushing teeth or exercising. The result? A family better prepared for financial challenges.

Resistance is natural. Some relatives will roll their eyes or say, “That’s not your business.” What can you do then? Start small. Offer a book instead of a lecture. Suggest an app instead of a judgment. Share your own struggles instead of giving commands. Remember: empathy opens doors that criticism closes.

Culture determines destiny. Families who integrate financial awareness into their daily rhythm set the stage for stronger futures. The cycle is powerful: children learn early, couples adjust habits, elders pass down wisdom. With each generation, literacy compounds like interest itself.

Imagine the impact. Imagine your great-grandchildren benefiting from the simple conversations you start today.

Helping family members build financial awareness is not about control—it’s about empowerment. Through transparency, shared resources, and real-life practice, families can transform money from a source of stress into a source of strength. The path is not linear, but it is rewarding.So start with a question tonight: What financial goal matters most to you this year? The answers may surprise you. More importantly, they may open the door to a legacy of literacy, resilience, and freedom.